Central banks back in the spotlight

Central banks back in the spotlight

More than a year after their accommodative pivot in the summer of 2024 following the decline in inflation, central banks, and the Fed in particular, are once again the main source of hope for investors in the coming months.

The Trump administration's main objective is to reindustrialize America. Such a process requires massive investment programs, both for businesses and for the federal government. The level of interest rates is therefore absolutely key. In this regard, the US key interest rate (+4.5%) appears far too high to carry out this ambitious program, and there is no doubt that the US administration is fully aware of this, in a context where the US budget deficit is over 6% and public debt exceeds 120% of GDP.

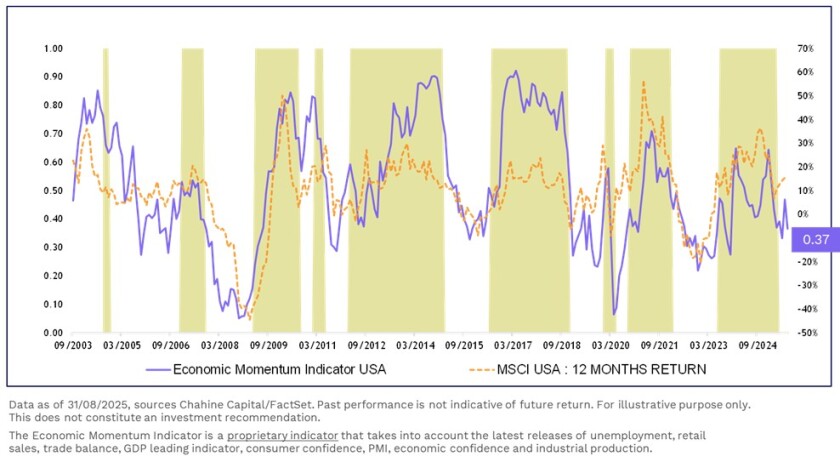

The slowdown in US economic momentum: a political choice?

The slowdown in US economic momentum is clear, unlike what we are seeing in Europe. Donald Trump's policies have contributed significantly to this, and the endless saga of tariffs has clearly weighed on the economic situation and general sentiment among economic agents on the other side of the Atlantic. It is only a short step from there to thinking that this is a deliberate move to force the hand of the US Federal Reserve and encourage it to return to an accommodative monetary cycle... and we dare to take that step!

Moreover, the US president has made no secret of his dissatisfaction with the Fed and its chairman Jerome Powell, whom he considers too slow to react, expressing his views publicly and with unprecedented aggression.

A Fed that is too restrictive

The Fed's key interest rate has remained stable at +4.5% since the last rate cut in December. With inflation at +2.9%, this means that the real key interest rate is +1.6%. This is very high compared to the average real key interest rate in the US since 2005, which is around -0.5%. But also compared to what is being implemented in the eurozone by the ECB, where the key rate has been lowered to 2%, with inflation at its target level of 2%, giving a real key rate of 0%.

It would therefore be logical for the US Federal Reserve to initiate a new cycle of rate cuts at its next monetary policy meeting on September 17.

This is particularly true given that the slowdown in US economic momentum is reducing the risk of a resurgence in inflation. Investors in inflation-linked bonds are forecasting inflation of 2.7% in the US in a year's time, down from its current level of 2.9%.

One central bank may hide another

The positive surprise could come from the ECB. While inflation in the eurozone has been hovering around its 2% target for several months, the rise of the euro, the introduction of customs tariffs, and the slowdown in economic momentum could cause inflation to fall. This is the view of investors in indexed bonds, who are anticipating German inflation of -0.05% over three years.

In such a context, the ECB may have no choice but to follow the Fed's accommodative lead if the latter were to initiate a cycle of rate cuts to counteract the risk of the dollar becoming even cheaper and reaching levels that could be potentially fatal for the European economy.

Opinion piece by Stéphane Levy, Strategist and Head of Innovation at IRIVEST Investment Managers, for l'Agefi.

Of investment

news and perspectives

Continue reading

.png)