2025 Review & 2026 Outlook

Dear investors,

IRIVEST Investment Managers was born out of the merger between Chahine Capital and DYNASTY Asset Management, with a clear ambition: to consolidate our resources while preserving the integrity of the expertise that makes them unique. This merger was built around a simple principle: to retain the DNA, teams, investment philosophies, and investment processes in order to ensure the continuity our clients expect.

In this context, our offering remains structured around complementary and transparent investment solutions: convertible bond and credit investment within DYNASTY SICAV, and quantitative momentum equity investment through our SICAV Digital Funds.

This dynamic is also reflected in a brand change, designed to better harmonize and clarify our range of Equity funds: the “Digital Funds” SICAV becomes “Chahine Funds,” and its sub-funds are renamed (Chahine Funds – Equity Europe, Equity Continental Europe, Equity Europe Smaller Companies, Equity Eurozone, Equity US).

This is solely a name change: the investment objectives and characteristics of the funds remain unchanged, with no action required on the part of investors.

Chahine Funds Equity range: 2025 review

After a positive first half dominated by strong upward trends in the Defense and Finance sectors, the second half continued the momentum, with a rally in commodities. Over the year 2025, the MSCI Europe NR index rose by +19.4% in EUR. The MSCI USA NR ended the year up +17.3% in USD, with a 13% differential between the euro and the dollar over the period.

Against this backdrop, our European Equity strategies benefited from these strong trends thanks to their sector positioning and the model's ability to select stocks in line with the themes of the year. They ended the year outperforming their respective indices.

Chahine Funds Equity Europe

The fund rose 24.4% over the year (Acc shareclass, EUR), outperforming its index by 5.0%.

Past performance is not indicative of future returns.

The year 2025 was dominated by the theme of Sovereignty, particularly in terms of Defense (Rheinmetall, Kongsberg), and by the revaluation of undervalued assets, which was particularly strong in the Banking sector (BPER, Banca Mediolanum). The rally in Metals (Fresnillo, Pan African Resources) continued into December, to the point where the sector ultimately contributed most to outperformance in 2025. The underweighting of the defensive Healthcare and Consumer Staples sectors also contributed positively in relative terms. Conversely, Technology and Travel/Leisure weighed on the fund, particularly at the end of the year.

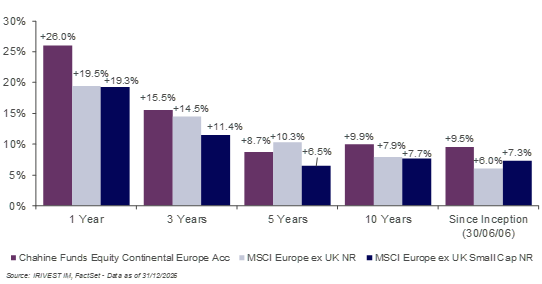

Chahine Funds Equity Continental Europe

The fund rose by +26.0% over the year (Acc shareclass, EUR), outperforming its index by +6.5%.

Past performance is not indicative of future returns.

The year 2025 was dominated by the theme of Sovereignty, particularly in terms of Defense (Rheinmetall, Kongsberg), and by the revaluation of undervalued assets, which was particularly strong in the Banking sector (BPER, Société Générale, BPM). The Materials sector continued to stand out in December, particularly in Chemicals (Alzchem). The underweighting of the defensive Healthcare and Consumer Staples sectors also contributed positively in relative terms. Conversely, Technology and Real Estate weighed on the fund, particularly at the end of the year.

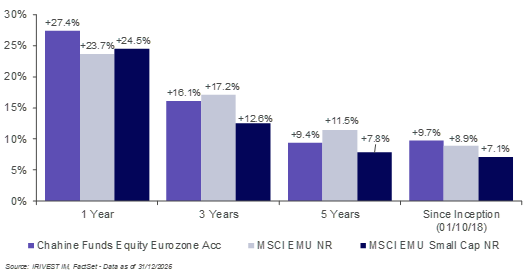

Chahine Funds Equity Eurozone

The fund rose 27.4% over the year (Acc shareclass, EUR), outperforming its index by 3.7%.

Past performance is not indicative of future returns.

2025 was a year of strong outperformance for the fund, driven by themes such as the quest for Sovereignty, particularly in Defense (Indra Sistemas) and Electricity Generation (Siemens Energy, Grenergy Renovables, Solaria), and the revaluation of undervalued assets, particularly in the Financial sector (BPER, Erste Group Bank, Unicaja Banco, etc.). The underweighting of the defensive Consumer Staples sector also contributed positively in relative terms. Conversely, the Real Estate sector weighed on performance.

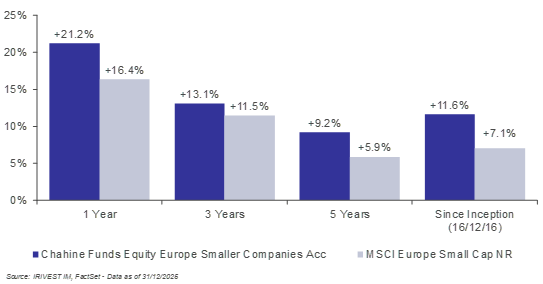

Chahine Funds Equity Europe Smaller Companies

The fund rose 21.2% over the year (Acc shareclass, EUR), outperforming its index by 4.9%.

Past performance is not indicative of future returns.

The year 2025 will have been marked by the theme of sovereignty, particularly in terms of Defense (Exail Technologie, HENSOLDT), and by the revaluation of undervalued assets, which had a particularly strong impact on Banks (BPER Banca, BAWAG, Unicaja Banco). The rally in Metals (Fresnillo, Pan African Resources) at the end of the year made this one of the sectors that contributed most to the fund's performance. Conversely, Technology weighed on the fund, particularly at the end of the year.

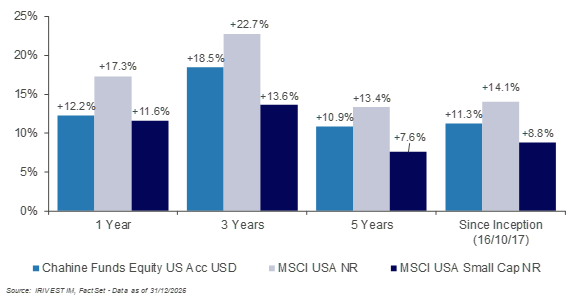

Chahine Funds Equity US

The fund rose 12.2% over the year (Acc USD share), compared with 17.3% for the MSCI USA NR and 11.6% for the MSCI USA Small Cap NR.

Past performance is not indicative of future returns.

The Technology sector benefited from massive investments in AI throughout the year, and although the fund was underweight in the sector, it was able to capitalize on the excellent performance of a few stocks (Western Digital, Lam Research, KLA). Furthermore, over the year, overexposure to small and mid-cap stocks, as well as financial sector stocks, had a negative impact on the fund, which ended up between the MSCI USA and the MSCI USA Small Cap.

Focus sur Chahine Funds Equity Europe

Two themes dominated the European equity market in 2025: the revaluation of undervalued assets and the quest for Sovereignty (whether in terms of the Economy, Defense, or Resources).

Certain undervalued sectors returned to their structural levels. The Financial sector benefited from this, particularly Banking, which continued its momentum from the previous year and ended the year up 75%. The Financial sector was heavily represented in the fund, through Banking (BPER Banca, NatWest, Banco BPM), Insurance (Unipol Assicurazioni) and other Financial Services, which had a positive impact on the fund's performance, both in absolute and relative terms. It should be noted that certain Italian Financial stocks also benefited from the sector's consolidation.

In terms of Economic Sovereignty, it was President Trump's imposition of tariffs in the United States that took the world (and the markets) by surprise. These had a negative impact on European Export sectors and a positive impact on more “Domestic” stocks. During this period of negotiations, the fund performed well thanks to its lower exposure to the United States than the market.

Next, military sovereignty led to an explosion in Defense spending in the first half of the year, against an already tense geopolitical backdrop. The Defense sector was heavily represented in the fund and even overweight compared to the market, which contributed significantly to the fund's performance thanks to stocks such as Rheinmetall, Kongsberg Gruppen, and MilDef.

Resource sovereignty created a marked trend in Mining and Metals in the second half of the year. The surge in gold prices, after a pause during the summer, propelled Fresnillo and Pan African Resources to the top of the fund's list of best contributors.

These notable trends during the year contributed positively to the fund's performance, thanks to its overweighting in the Materials, Finance, and Defense sectors. The fund's favorable positioning was also reflected in its underweighting in Defensive sectors such as Healthcare and Consumer Staples, which ended the year on a mixed note compared to the market.

Conversely, the Technology sector weighed on the fund, as did Travel and Leisure, particularly at the end of the year.

Finally, another notable feature of the fund was the triggering of one of our three “inflexion point smoothing tools” on July 1st. These mechanisms are designed to detect the risk of overheating of the momentum factor, which is at the heart of our equity strategies. They are typically not triggered more than every three to five years. When triggered, the list of stocks selected in the portfolio was modified with the aim of reducing active risk: total or partial sale of the most polarizing stocks that put us at risk, and selection of “anti-momentum” stocks that serve to reduce this active risk. Unsurprisingly, the stocks that were removed were mainly in the Defense and Finance sectors. To replace them, our selection included “anti-momentum” stocks from sectors such as Consumer Staples (Barry Callebaut), Luxury Goods (Kering), Healthcare (GSK), etc. We estimate that this procedure had a positive impact of around +1.2% on the fund's performance.

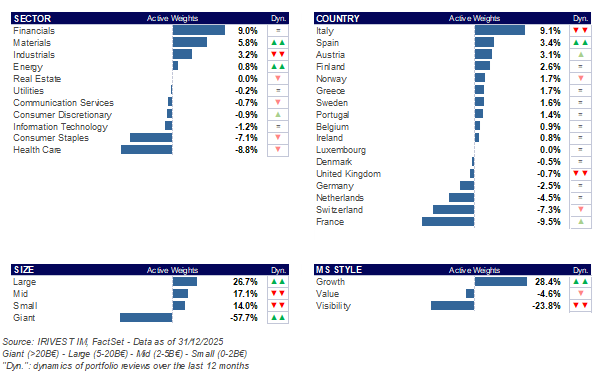

Relative positioning of the fund (vs. MSCI Europe NR)

These breakdowns are not constant and may change over time.

According to our Economic Momentum indicator, we are still in a procyclical environment, which is generally favorable to cyclical assets. This explains why the fund is still overweight in small and mid caps.

During the year, the main changes in sectors concerned:

- Industry, which was reduced. The move was initiated mainly on Defense-related stocks on July 1st when our “smoothing tool” was triggered. Subsequently, the model took over and continued to reduce the overweight position in the Industrial sector.

- Finance, which was also reduced during the year, but returned to its initial level following the continuation of the trend in this sector.

- Materials, which are now significantly overweight, particularly Mining and Metals.

In geographical terms, Italy remains heavily overweight, despite being reduced during the year, and France is still the most underweight country.

Convertible bonds: 2025 review and 2026 outlook

The year 2025 will go down as an exceptional year for convertible bonds, with the asset class delivering returns of over 20% for the global universe. This outperformance can be explained by the favorable combination of three factors: a buoyant macroeconomic environment characterized by resilient growth and gradual disinflation, exceptional technical market conditions with record issuance volumes and liquidity, and sector exposure aligned with long-term structural trends such as Artificial Intelligence, Energy Transition, and Defense Modernization.

We are entering 2026 with confidence, even though political and geopolitical risks remain. The environment remains favorable for the asset class, with monetary easing expected from the Federal Reserve and solid fundamentals. We anticipate a return to solid but more moderate performance. This moderation is part of a natural consolidation process after an exceptional year, while preserving the attractiveness of the asset class in terms of risk-adjusted returns.

Our positioning favors a balanced approach combining credit quality and selective exposure to high-potential growth themes. We are maintaining a defensive stance with a bias towards solid bond floors with short durations, while capitalizing on investment opportunities in three strategic areas: Artificial Intelligence, Energy Transition and Defense System Modernization. This strategy aims to optimize the risk/return profile in a market environment that remains buoyant but whose potential volatility requires discipline and selectivity.

2025 review: a record year in a buoyant environment

2025 was marked by a macroeconomic realignment that was particularly favorable to growth assets. After two years of restrictive monetary policy, the Federal Reserve began a cycle of easing in the second half of the year, with market expectations now pricing in three to four rate cuts for 2026. This shift comes amid gradual disinflation, with core inflation returning to a trajectory consistent with the Fed's 2% target, without compromising Economic Growth Momentum.

Global growth stood at around 2.5% in 2025, supported by two powerful drivers: on the one hand, the massive investment cycle in Artificial Intelligence infrastructure and, on the other, US consumption, which remained resilient despite high interest rates for most of the year. This macroeconomic configuration of moderate growth, controlled inflation, and accommodative monetary policy is the ideal environment for convertible bonds, which benefit simultaneously from bond carry and participation in the upside potential of the underlying equities.

The credit market was characterized by a continued compression of spreads, with high-yield risk premiums standing at 270 basis points at the end of the year, a historically low-level reflecting both abundant liquidity and solid corporate fundamentals. The proportion of distressed issuers fell below 1%, its lowest level since 2021, reflecting a particularly healthy credit environment.

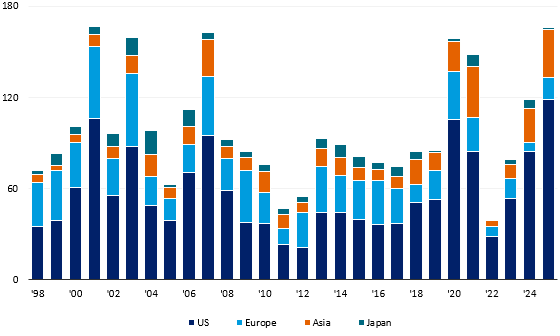

The year 2025 saw the primary and secondary markets for convertible bonds reach unprecedented levels of activity, structurally transforming this asset class.

Primary market: $166 billion in 2025

Global convertible bond issuance reached $166 billion in 2025.

Source: BoFa, data as of 23/01/2026.

This exceptional dynamic can be explained by three converging factors.

Firstly, attractive equity valuations made convertible bond issuance particularly advantageous for issuers, enabling them to raise capital at favorable coupon rates averaging 2.5-3.0%, while limiting immediate shareholder dilution. Second, the massive investment cycle in Artificial Intelligence has required significant fundraising to finance infrastructure, with technology companies accounting for nearly 70% of US issues. Thirdly, a significant wall of maturities worth $145 billion coming due between 2026 and 2028 generated a wave of early refinancing under favorable market conditions.

The geographical breakdown of issues reveals continued US dominance with more than $119 billion, followed by Asia excluding Japan with $33 billion and Europe with $14 billion.

The secondary market also saw remarkable activity with record volumes. This structural improvement in liquidity has been accompanied by a significant broadening of the investor base. Long-only funds returned to inflows in the third quarter of 2025 after two consecutive years of outflows, signaling renewed confidence among institutional investors. At the same time, hedge funds dedicated to convertible arbitrage increased their assets under management, creating greater capacity to absorb new issues.

In this exceptional environment, our global convertible strategy captured most of the asset class's performance while maintaining strict discipline on the risk profile. Our defensive approach, characterized by an investment grade bias and controlled equity sensitivity of between 20% and 40%, enabled us to participate in the rise of the underlying equity markets with fund volatility of 5%.

Our sector positioning contributed positively to performance, with significant exposure to Semiconductors and Cloud Infrastructure via positions in SK Hynix and Wiwynn, to the Defense sector with Rheinmetall, AeroVironment, and Parsons, and to next-generation Utilities positioned for the Energy transition, such as Nextera Energy. These thematic convictions proved particularly promising in an environment marked by the acceleration of the investment cycle in AI and European rearmament.

Outlook for 2026: opportunities in a normalized environment

For 2026, we anticipate a broadly constructive macroeconomic environment for convertible bonds, although less uniformly favorable than in 2025. Economic growth rates are expected to converge towards their long-term trend of around 2% globally, supported by continued investment in digital infrastructure and resilient consumption, but facing risks related to trade policies and potential geopolitical tensions.

The main macroeconomic support will come from monetary policy. The Federal Reserve is expected to continue its easing cycle, with three to four rate cuts anticipated by the consensus, bringing the Fed Funds rate close to 3% at the end of the year. This easing of financial conditions is favorable for convertible bond issuers with high sensitivity to growth.

The short duration characteristic of convertible bonds, averaging around two years, is an advantage in this context, allowing investors to capture the benefits of rate compression while limiting exposure to duration risk in the event of a resurgence of inflation. At the same time, credit spreads in the high-yield market offer a risk premium that remains adequate given the low distress rate and the prospects for earnings growth among issuers.

Nevertheless, we identify four macroeconomic risks to watch out for in 2026: the risk of a speculative bubble in AI-related stocks, the risk of imported stagflation via aggressive tariff measures, the risk of a delay in the monetary easing cycle in the event of persistent inflation, and idiosyncratic credit risk in a context of stretched valuations.

Relative valuation analysis is one of the most compelling arguments in favor of convertible bonds for 2026. After a year of strong performance, the asset class remains attractive in terms of valuation, both in absolute terms and relative to equities and traditional credit.

Source: Jefferies

Convertible bond issuers trade on average at multiples of 13 to 16 times projected earnings, with revenue and EBITDA growth prospects of 13% to 19%, significantly higher than the average for equity indices. By way of comparison, the S&P 500 index was trading at a multiple of 25 times one-year earnings at the end of 2025, with expected growth of 8% to 10%. This structural discount reflects the sector composition of the convertible universe, which is geared towards mid-cap growth companies rather than the mega-caps that dominate traditional equity indices.

Compared to traditional bonds, convertibles have a significantly more favorable credit risk profile. The historical default rate for convertible bonds is around 1% per year, compared to more than 3% for comparable high-yield bonds. This greater resilience can be explained by several structural factors: an issuer base focused on growth rather than mature cyclical sectors, often greater financial discipline on the part of developing companies keen to preserve their access to the market, and a capital structure that encourages conversion rather than default when equity valuations rise.

Finally, the convertible bond universe has a sector distribution that is one of its main attractions for institutional investors seeking exposure to major structural trends without the full volatility of the equity markets.

The Technology sector, including Semiconductors, Software, and Cloud Infrastructure, accounts for half of the US convertible universe. This high weighting reflects the capital intensity of these industries and their structural use of convertibles as a financing instrument. The growth outlook remains robust, with revenue growth expected to range from 13% to 19%, driven by several catalysts: the ongoing investment cycle in AI, estimated at $600 billion in 2026; the widespread adoption of AI in enterprise applications; and the deployment of infrastructure.

The Industrial sector, including Defense, accounts for 15% of the US market, with growth prospects of 6% to 10%. The main catalysts come from the Trump administration's defense modernization programs, but also from Europe, with a German budget of €52 billion.

Conclusion

The year 2026 begins with favorable fundamentals for convertible bonds, combining macroeconomic support with monetary easing and resilient growth, solid technical conditions with a dynamic primary market, and exposure to long-term structural themes such as Artificial Intelligence, Energy, and Defense. Our approach for the coming year favors discipline and selectivity, combining protection through high-quality credits and growth opportunities through high-potential thematic convictions.

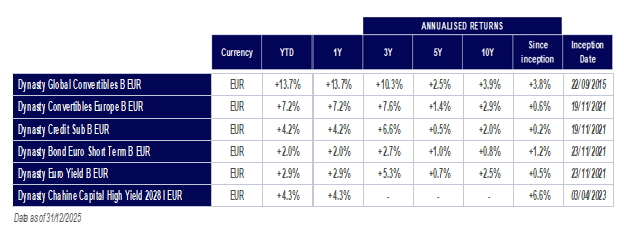

Dynasty Fund Performance

Past performance is not indicative of future returns. Source: FactSet / IRIVEST IM.

Macro Outlook:

The initial year of Donald Trump's second term has not been an easy one for investors, but there is no doubt that they will nevertheless look back on it fondly. The MSCI Europe NR index rose by +16.3% in euros and the MSCI USA NR index by +17.3% in US dollars (+3.4% in euros). At the same time, the profound transformation of political and geopolitical standards has led to the emergence of strong trends that are particularly favorable to momentum investing.

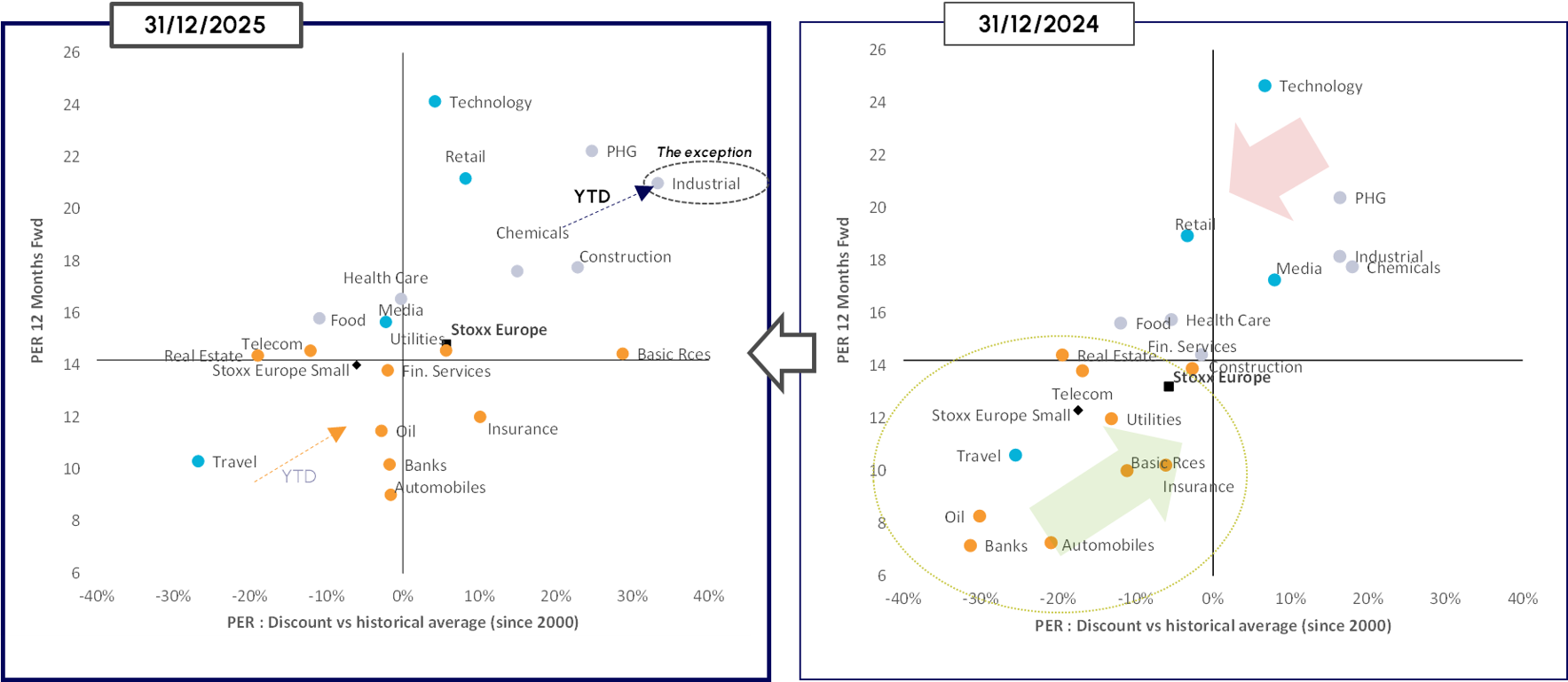

Fundamental normalization and sovereignty drove European stock markets in 2025

In Europe, almost all Value sectors and the Industrial sector posted returns of over 20%.

Data as of 31/12/2025, ex dividends. Source FactSet / IRIVEST IM, *MultiSmart Proprietary indices.

The re-rating of European value stocks is part of a healthy fundamental normalization process whereby the various segments of the market are converging towards their standard historical valuation levels.

The catalyst for this normalization process was undoubtedly the sharp decline of the dollar against the euro in 2025, which weighed relatively heavily on Export sectors in Europe and, conversely, supported sectors with a “Domestic” profile. These “Domestic” sectors are all Value sectors (e.g., banks, insurance, utilities).

This normalization process remedied a fundamental situation which, a year ago, revealed a clear undervaluation of the value segment, as we highlighted in our January 2025 semi-annual letter.

Data as of 31/12/2025. Source FactSet / IRIVEST IM.

The graph above perfectly illustrates this fundamental normalization observed in 2025. A year ago, only value sectors were trading at a discount to their historical standard, but this is no longer the case following their sharp rise in price.

The theme of sovereignty can be illustrated by the rise in price of the Industrial sector. This broad sector, which includes a large number of companies involved in the Defense industry and committed to Energy independence, also rose sharply in 2025, driven by announcements of massive investment plans in Europe, reaching unprecedented valuation levels in both absolute and relative terms.

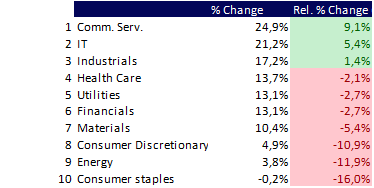

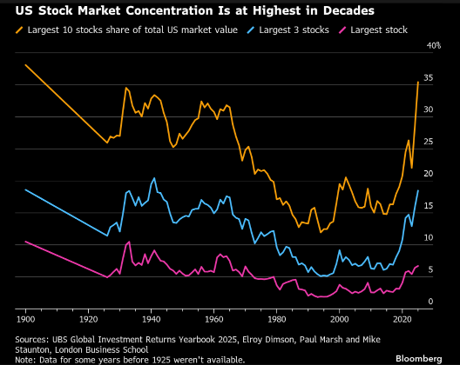

US market: GAFAM in concentrated form!

In the United States, the dynamic is quite different. GAFAM continued to drive the indices, exacerbating market polarization in terms of valuations. The Telecommunications Services and Technology sectors, particularly thanks to the Semiconductor sub-sectors, continued to stand out.

2025 return of US sectors

The weight of GAFAM stocks within the US index has reached unprecedented levels in history.

This unprecedented concentration highlights a paradoxical situation in the United States. While the S&P 500 index is trading at a record premium to its historical average valuation levels, the majority of listed US companies are trading at a discount.

The S&P 500 is currently trading at a premium of more than 30%, while the MSCI USA Small Caps index is trading at a discount of nearly 6%.

Data as of 31/12/2025. Source FactSet / IRIVEST IM.

Outlook for 2026: Central Banks are in the spotlight

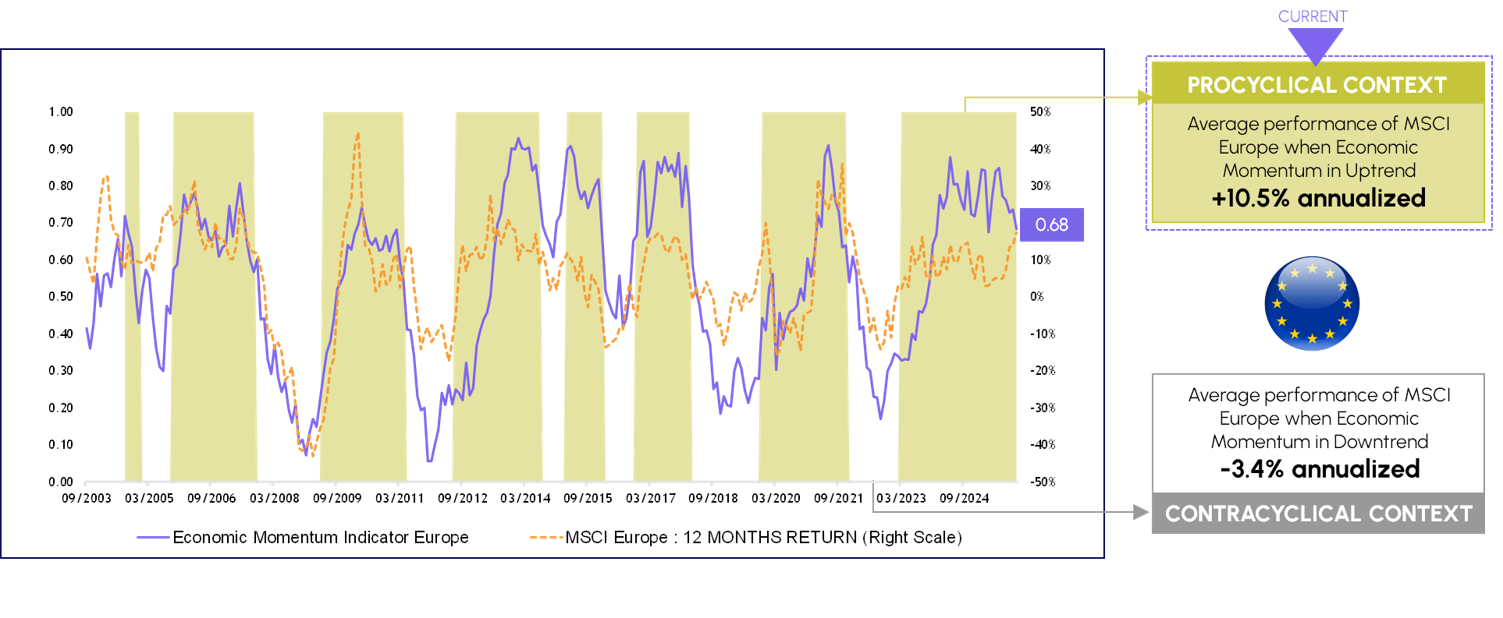

Since fall 2022, European stock indices have risen by around 60%, and as we enter 2026, it is legitimate to question the sustainability of this rally after such a buoyant and prolonged period.

The economic cycle is what drives stock market performance over the long term. The chart below illustrates this perfectly. It highlights the consistent correlation between our proprietary economic momentum indicator and market dynamics in Europe.

Data as of 31/12/2025, source FactSet / IRIVEST IM. Past performance is not indicative of future results. For illustrative purpose only. This does not constitute an investment recommendation. The Economic Momentum Indicator is a proprietary indicator that takes into account the latest releases of unemployment, retail sales, trade balance, GDP leading indicator, consumer confidence, PMI, economic confidence and industrial production.

Our indicator has been in expansionary territory since March 2023 (shown by the green bands on the graph), a record duration since its inception in 2003. In a “normal” context, it would not be surprising to see a shift in the first half of 2026 signaling a less favorable economic environment for European equities. This is especially true given that economic momentum in the United States, the world's largest economy, has been showing serious signs of losing steam since last spring.

Nevertheless, we cannot rule out the possibility that this bullish stock market cycle will be prolonged by strong monetary accommodation.

After taking a back seat for most of 2025, central banks are now returning to center stage. The Fed restarted a cycle of rate cuts in September in response to the significant deterioration in US economic momentum. This deterioration was caused by Donald Trump's trade policy, the primary goal of which, in our view, was to force the Fed to cut rates. Mission accomplished!

The market anticipates further rate cuts by the Fed in 2026. Two or three 0.25% cuts in the Fed Funds rate are currently anticipated.

We are expecting four cuts in the United States, for four reasons:

- Inflation in a year's time should ease to around 2.3% (vs. 2.7% currently) if we are to believe US inflation break-even rates.

- The real Fed Fund rate stands at +1.0% compared to an average of -0.8% since 2002, highlighting a monetary environment that is still too restrictive and seen by the Trump administration as a hindrance to the country's reindustrialization.

- The appointment of a new Fed Chair to replace Jerome Powell. Whether it is Kevin Hassett, Kevin Warsh, or another likely candidate, there is no doubt that the successful candidate will adopt an accommodative monetary policy in line with the new administration

- Finally, on a more structural level, the productivity shock enabled by AI could justify a sustained accommodative bias by the Fed, whose mandate includes supporting employment.

Such a scenario could allow the small- and mid-cap US equity segment to extend its relative recovery (compared to the S&P 500 and GAFAM) that began last February.

Data as of 06/01/2026. Source Bloomberg / IRIVEST IM.

In this context, the ECB could soon deliver a surprise. After bringing the deposit rate (2.0%) down to the level of inflation (2.1%), it has been holding steady since last June. If this pause continues, as is currently anticipated, it could pose a major risk to the European economy in the form of a sharp appreciation of the euro.

We therefore believe that the ECB could surprise us and come out of the woodwork by lowering key interest rates. This is all the more likely given that inflationary risks appear negligible in a context of sluggish growth, a weak dollar and low oil prices, as confirmed by inflation break-even rates in Europe, which point to deflation in Germany over the next three years.

Data as of 02/01/2026. Source Bloomberg / IRIVEST IM.

This is a scenario that the bond market is not yet anticipating at this stage, and one that could give a second wind to European economic momentum, the equity market, and its cyclical components, including small and mid caps.

A well-positioned bond market

We continue to believe that the yield curve steepening process could continue on both sides of the Atlantic, thanks in particular to the easing of the short end, which is more sensitive to monetary policy shifts.

Carry strategies should continue to perform well, as should credit markets, despite the significant contraction in spreads. For example, the European Markit High Yield 5-year CDS index currently shows a spread of 330 bps, compared with a historic low of 270 bps.

However, public debt levels are such that corporate spreads could continue to narrow (due to the deterioration in sovereign risks).

In this context, convertible bonds could continue to perform well after a record year for new issues in 2025. This hybrid asset class provides access to long-term optionality, against a backdrop of still reasonable equity valuations in many segments, low risk of rising interest rates and downward pressure on credit spreads.

________________________________________

ABOUT IRIVEST INVESTMENT MANAGERS : www.irivest.com

IRIVEST Investment Managers is an independent Luxembourg-based investment management company. Since 1998, it has been a pioneer in quantitative momentum investment applied to European and US equity strategies through the “Chahine Funds” SICAV. The equity investment team develops algorithmic models to identify stocks that will outperform the market. Its expertise in convertible bond and credit investment with “DYNASTY SICAV” is characterized by non-benchmarked investment based on strong convictions and a bottom-up selection process. IRIVEST Investment Managers is a member of IRIS Finance International Group and is based in Luxembourg and Paris.

DISCLAIMER

It is the reader's responsibility to evaluate and assume all risks associated with the use of the information contained in this document, including the risk of reliance on the accuracy, completeness, security, or usefulness of this information. The content of this document is published for informational purposes only and should not be construed as financial or other advice, or as an offer to sell or a solicitation of an offer to purchase securities in any jurisdiction where such an offer or solicitation would be unlawful. Please refer to the prospectuses and key information documents before making any final investment decision. Any information expressed in this document as of its date of publication is subject to change without notice. The opinions or statements contained in this document do not represent the opinions or beliefs of IRIVEST Investment Managers. IRIVEST Investment Managers and/or one or more of its employees or editors may hold a position in any of the securities mentioned in this document.

Of investment

news and perspectives

Continue reading

.png)